Sign up to keep up-to-date

For those wishing to receive about monthly updates or to volunteer as a signatory on the demand letter/lawsuit we are preparing for the Whitman County Assessor, please submit your info below.

This site will be updated as we gather more information. Last updated July 31, 2024 with information about the county’s decision on their plan to do nothing and updates with some data analysis of county assessment and taxation data.

The slides from the April 1 meeting can be downloaded from this link.

Overview

Many in the city of Pullman have seen their property taxes increase 15-200% in 2024. This includes virtually everyone on Pioneer Hill and Sunnyside Hill. It also includes some others throughout the city, most often those who made a purchase in the 2020-2022 timeframe and hadn’t been revalued since 2015.

You may have even contacted the County Assessor’s Office and been given an explanation that satisfied you and you were now trying to figure out how to pay for it. This website is to describe in detail why this happened, and begin the process to correct what we believe is a grave mistake. The key takeaways from everything below should be the following:

- THIS IS NOT A TAX INCREASE ON THE COUNTY AS A WHOLE.

- EACH TAX DISTRICT, BY STATE LAW, IS ONLY ALLOWED TO INCREASE TAXES BY 1% PER YEAR.

- THIS IS A PROBLEM WITH THE REVALUATION PROCEDURE THAT IS MAKING THOSE WHO WERE REVALUED THIS YEAR PAY AN OUTSIZED PORTION OF THE TAXES.

History

There are state laws that are important to this discussion:

- Washington State mandates that all properties be revalued at 100% of actual value.

- Washington State mandates that physical inspection be done at least every 6 years.

- Wahsington State mandates that revaluation be done every year.

- Washington State only allows non-voted-on property taxes collected by each taxation district to go up by 1% annually.

Whitman County has been not good, to put it mildly, at adhering to those first three mandates. There are many, many properties in the county that are currently assessed at 30-50% of their actual value. Furthermore the state government has been demanding that counties expedite the process of bringing assessed values up to actual values.

The Problem

So from the start, we can rule out that there has been a large county-wide tax increase. That isn’t allowed by state law for non-voted-on property taxes, and for Pullman there hasn’t been a vote-on property tax increase for this year. Each tax district that you belong to — hospital, school, county — is likely taxing at their 2023 amount plus 1%. So for one person on the south side of Pullman to see a $4000 tax increase and many people on the south side of Pullman and elsewhere in the county see a $500 tax decrease, it is obvious there is something else that is amiss.

When we saw this disparity, we called the County Assessor to investigate the problem. During those phone calls we discovered the following details:

- These portions of Pullman were the first group subjected to the effort to bring assessed property values up to 100% actual value.

- The assessors revaluation plan is to first bring assessed values up 80% of actual value during a 6year cycle, with a second 6-year cycle to to bring assessed property values up to 100% of actual value.

The root of the problem is that a small portion of the county was revalued at these much higher values, thus shifting the ratio of these two sections relative to the sum total of all assessed values. The tax districts aren’t collecting more taxes, it is just that those who have been revalued at 80% of actual value are paying a larger percentage of the total revenues of the tax district.

Expand this section to show a spreadsheet that completely illustrates how this rapid catchup to actual values punishes those first assessed.

Can the County Assessor Do This?

We believe the answer is a resounding: “No!”

What the State Law Says

- “RCW 84.40.030 (1) All property must be valued at one hundred percent of its true and fair value in money and assessed on the same basis unless specifically provided otherwise by law.”

- The lack of historical adherence to this law has created a situation where one group is taxed unequally, even in the presence of a systematic process for physical inspection going forward.

- Furthermore, Area 6 (Sunnyside Hill and Pioneer Hill) was arbitrarily chosen to go first in this unequal process. No other areas of the county were revalued (Except for some houses that sold in the 2020-2022 range throughout the county).

- “RCW 84.41.030 (1) Each county assessor must maintain an active and systematic program of revaluation on a continuous basis. All taxable real property within a county must be revalued annually, and all taxable real property within a county must be physically inspected at least once every six years.”

- Even in the current year, the assessor did not adhere to the law that “all taxable real property within a county must be revalued annually”. It appears that both historically and continuing that revaluation only occurs on a year with a physical inspection.

- This point was one that was identified in the Department of Revenue 2023 Audit of the Whitman County Property Tax Administration as a “Required” correction and wasn’t accomplished:

“The law requires the Assessor to update assessed values on parcels in the areas of the County not scheduled for physical inspection in a given year. The Assessor should update the assessed value of all parcels in the County to reflect the current market value, unless market data indicates that no change in market value has occurred year to year”

What Case Law Says

There are a variety of United States and Washington State Supreme Court cases in which unfair taxation has been ruled as a violation of the Equal Protection Clauses of both the federal and state constitutions. The most pertinent cases to our situation seem to be

- Sioux City Bridge Co. v. Dakota County, 260 U.S. 441 (1923)

- Allegheny-Pittsburgh Coal Co. v. County Comm’n, 488 U.S. 336 (1989)

- Dore v. Kinnear, 79 Wn.2d 755, 489 P.2d 898 (1971).

In the Sioux City… case, near the end of the decision, the majority opinion states that they can’t compel a county to reassess all properties because it is a timely process. However, the decision also says that when timely reassessment isn’t possible or adhered to, that the taxpayer should only be taxed at the same level as their peers until such a time that assessments result in equality:

The conclusion in these and other federal authorities is that such a result as that reached by the Supreme Court of Nebraska is to deny the injured taxpayer any remedy at all because it is utterly impossible for him by any judicial proceeding to secure an increase in the assessment of the great mass of underassessed property in the taxing district. This Court holds that the right of the taxpayer whose property alone is taxed at 100 percent of its true value is to have his assessment reduced to the percentage of that value at which others are taxed even though this is a departure from the requirement of statute. The conclusion is based on the principle that, where it is impossible to secure both the standard of the true value, and the uniformity and equality required by law, the latter requirement is to be preferred as the just and ultimate purpose of the law. (emphasis added)

Sioux City Bridge Co. v. Dakota County, 260 U.S. 441 (1923)

Later cases, such as the Allegheny-Pittsburgh… case further gave further leeway to assessing authorities such that if they have a systematic process that doesn’t overly burden a taxpayer on average over the period of the systematic assessment process unfairly compared to their peers, in a manner that is “arbitrary, capricious, or intentional”, then they can be said to have met the standard of “equal protection under the law”. Even a memo from the Washington State Attorney General’s office from 1992 (link) cited this case and described how very specific conditions must be met in order for the Equal Protection standard to be satisfied:

“The United States Supreme Court likewise has addressed the issue of regularity in assessment systems in Allegheny Pittsburgh Coal Co. v. Webster Cy., 488 U.S. 336, 102 L. Ed. 2d 688, 109 S. Ct. 633 (1989). The taxpayers inAllegheny owned real property suitable for coal mining. The Webster County Assessor had a practice of assessing recently sold properties at current market value and making only minor adjustments to properties that were not sold. This practice had resulted in assessment and tax rates that were approximately 8 to 35 times higher on recently sold properties than those applied to comparable neighboring properties that had not been recently sold. The practice was challenged as a violation of uniformity and equal protection. The United States Supreme Court agreed with the taxpayers that they had been denied equal protection because the assessor’s actions were not designed to result in equalizing the burden on comparable properties over time. In condemning this system, the court indicated what elements a proper reappraisal system would contain:

Authority of County Board of Equalization to Equalize the Assessment of Property, AGO 1992 No. 14 – Jul 15 1992, Attorney General Ken Eikenberry

As long as general adjustments are accurate enough over a short period of time to equalize the differences in proportion between the assessments of a class of property holders, the Equal Protection Clause is satisfied. . . . In each case, the constitutional requirement is the seasonable attainment of a rough equality in tax treatment of similarly situated property owners.” (emphasis added)

Attorney General Ekinberry’s memo continues to describe the Dore v. Kinnear… case from the Washington State Supreme Court regarding unfair taxation that occurred in King County:

The necessary elements for a valid cyclical revaluation process were further delineated in Dore v. Kinnear, 79 Wn.2d 755, 489 P.2d 898(1971). In Dore, the Washington Supreme Court struck down the King County Assessor’s valuations for the first year of a four-year cycle as a violation of the equal protection clauses of the state and federal constitutions and the uniformity provisions of the fourteenth amendment to the state constitution. The King County Assessor had revalued only six percent of the parcels within King county in the first year of a four-year cyclical process. The court contrasted this failure to approach the level of revaluation necessary to complete the process in a systematic four-year manner with the good faith efforts of the assessors in the Carkonen case. The court required, above all, that the process be systematic. (emphasis added)

Authority of County Board of Equalization to Equalize the Assessment of Property, AGO 1992 No. 14 – Jul 15 1992, Attorney General Ken Eikenberry

State law has changed since this memo and now requires all properties to be revalued at 100% of their actual value in each calendar year, but the principles and requirement set forth in these cases of “seasonable attainment of a rough equality in tax treatment of similarly situated property owners” are still necessary to ensure equal protections are guaranteed for taxpayers.

Update from 2024 Revaluation for 2025 Tax Year

Many of you on the north side of Pullman and elsewhere likely started to see your revaluation notices arriving in the mail. As expected, this hasn’t been fixed yet and the north side of Pullman was hit in a similar manner to the south side of Pullman last year, in which their property values were brought up to about 80% of their fair market value. It appears that the assessor made an attempt to placate concerns by conducting a 15% property value increase across almost all of the rest of residential properties in the county, leaving most of those at somewhere between 45% and 50% of actual value.

Here is a summary of what most people in the county likely experience over the last 2 years:

- If you were on the south side of Pullman or had a new build or new purchase anywhere in the county, you saw revaluation in 2023 to about 80% of fair market value (for the 2024 tax year)

- If you were on the north side of Pullman, or had a new build or new purchase anywhere in the county, you saw revaluation in 2024 to about 80% of fair market value (for the 2025 tax year)

- If you were elsewhere in the county, you saw revaluation in 2024 of almost exactly a 15% increase on land and close to 15% on improvement (for the 2025 tax year)

- If you were classified as “ag use” anywhere in the county, you were not revalues in 2023 or 2024.

Of course, there are some exceptions to this that were likely mistakes or oversights. Some of the mistakes/oversights that we found were:

- Most new purchases in 2022-2024 we inspected outside of Pullman, did trigger a revaluation, but it was not to 80% of fair market value. These were more than the 15% across the board increase, but averaged only about 50% of fair market value. New purchases in Pullman were revalued to 80% in 2022-2024, even if not in the active physical inspection area. In the cases that it wasn’t, they did receive the 15% increase in 2024 (for the 2025 tax year). There were a handful of new build and new sales we saw in Colfax where a new purchase had the <80% of fair market value applied in 2023 and still had the 15% increase in 2024.

- There was at least one pocket of homes on the south side of Pullman (on Alcora Dr) that was not revalued in 2023, and again wasn’t revalued in 2024. These didn’t even have the 15% increase that appears to have been applied across the board in the 2024 year to all non-Pullman properties.

- We couldn’t find any homes on the south side of Pullman that had the 15% across the board increase applied.

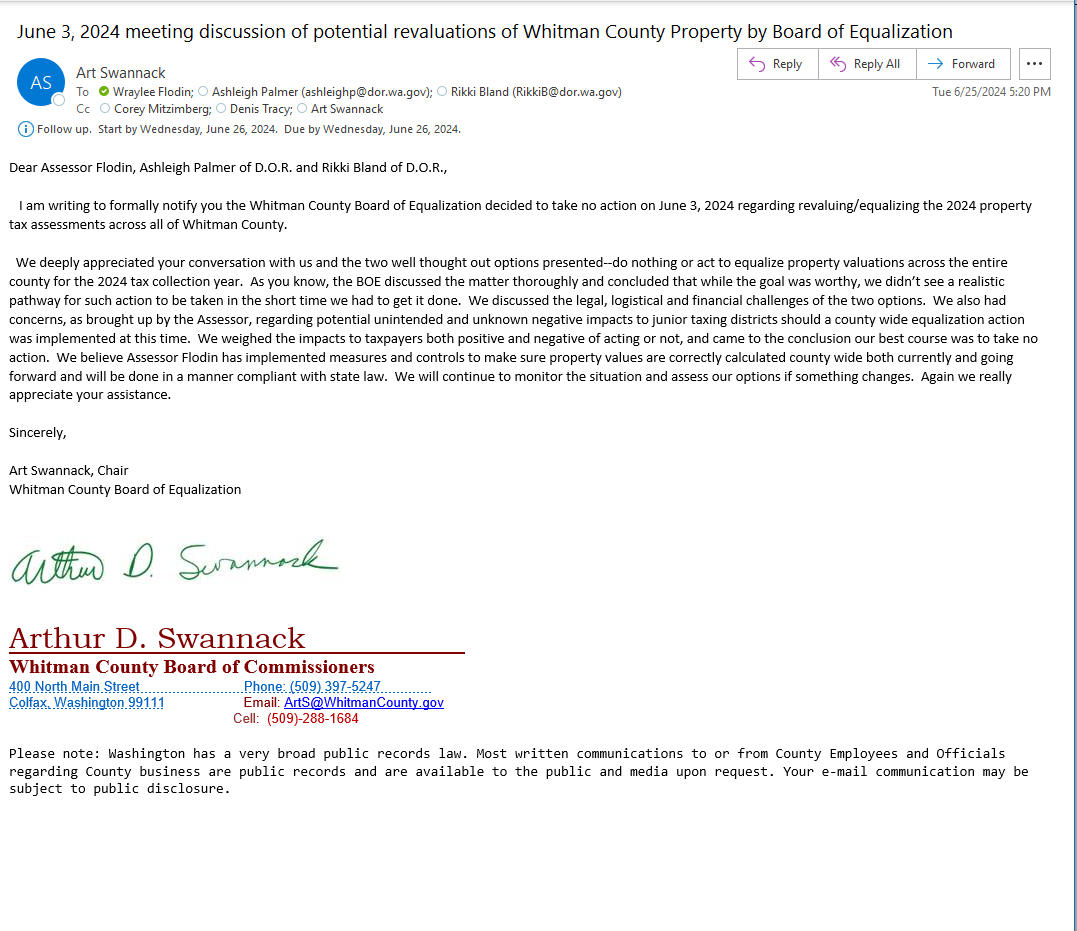

Update from County about their “No Action” Plan

The county has given a formal response, and it wasn’t good. The short version is that the county, despite having been explicitly told by the WA State Department of Revenue in an official exec to memo that they aren’t following the law, decided to do nothing to fix their mistake because they think the threat of a lawsuit is less work/cost and less bothersome than the steps to fix it.

Here is a summary of what we received from the county as part of their decision process (link files here and in the Downloads section below):

- An executive memorandum from the Washington State Department of Revenue (DOR)to the Whitman County Assessor and the Board of Equalization (essentially the county commissioners). The memo states that the assessor has not been following state law and continues to fail to follow state law. They give the assessor and Board of Equalization two options:

- No Action: the DOR warns them that this opens them to legal peril

- Equalize at least Pullman and preferably the whole county: they describe that this is a difficult process, but that resources are available to complete this.

- An email from the Board of Equalization (made up of the county commissioners) saying that the cost and complexity is too hard, and that they are taking the No Action option.

- An email from Assessor Flodin relaying this information to us.

{kind=link}

We are dismayed at the county’s decision to not follow the law and force a legal challenge to fix the obvious mistakes. You can see a much more thorough analysis of these three documents and the decision at Summary of Assessor Response.

Conclusions

The process taken by the county assessors constitutes and illegal revaluation plan

What the Law Says

- The plan violates state law

- Property must be valued at 100% of its true and fair value

- The County Assessor must maintain an active and systematic program of revaluation

- All property must be revalued annually

- The plan violates case law

- The plan must be orderly, not be arbitrary, capricious or intentionally discriminatory.

- Minor discrepancies will be tolerated.

- The plan requires reasonable attainment of a rough equality in tax treatment of similarly situated property owners.

- Substantially and equal amount of taxable property in a county be revalued each year to comply with the equal protection clauses of both the state and federal constitutions and the uniformity provisions of the fourteenth amendment to the state constitution.

What the County has Done

- It is arbitrary. There is no rationale for why this portion of the county was selected first, and the same unequal effect would have occurred for any portion of the county that was singled out and assessed far above their peers. It is possibly capricious, as the recent sales on other hills triggering assessments not done on nearby homes seems to target home with a new known assessment.

- The Whitman County assessment has been far from “systematic”. Even though the current County Assessment Plan is closer to what is required by law and is trying to implement a systematic process, prior failures to execute a systematic process and follow state law results in a situation of unfair taxation.

- Some people haven’t been reassessed for 14 years, while others have been on 6 year intervals.

- The state law standard for assessment of 100% of actual value has not been followed for decades (until now).

- Some people who hadn’t been reassessed for the past 9 years were reassessed this year, while others weren’t.

- Even the new plan doesn’t revaluate all properties each year, but instead every 6 years.

- The approach taken does not result in a tax burden that is approximately even over the systematic assessment process, even if a systematic process is adhered to going forward. It does not “[attain] a rough equality in tax treatment of similarly situated property owners” as required by the Supreme Court and cited as the standard by the Washington State Attorney General.

Plan of Action (updated July 2024)

Step 1: Make those who have been adversely affected aware of the problem. This is an ongoing process. Tell your friends and neighbors about this website. Get them

Step 2: Set up an attorney escrow account for donations for a lawsuit. This will fund the costs of a case in superior court and allow a mechanism for returning funds if lawyers fees are awarded in a successful suit.

Step3: Hold a drive to hand out flyers to garner large public support for another public meeting to kick off the legal process to force the county to fix the mistakes and follow state law and satisfy constitutional requirement for equal protection and uniformity in taxation.

Contact Info

For those wishing to have more info or to volunteer as a signatory on the demand letter we are preparing for the Whitman County Assessor, please contact John Swensen at jpswensen+taxissue@gmail.com

Downloads

- Understanding Property Taxes in Washington State (particularly as it applies to Whitman County)

- Slides from the April 1 meeting

- Whitman County Documents

- Assessor/Board of Equalization July 2024 Decision to Take No Action

- Washington State Documents

- Excel spreadsheet demonstrating the inequality in the current 12 year cycle of the 2023 Revaluation Plan

- Additional Case Law Supporting the Complaint – All were identified as successful court challenges that referenced the prior Dore v. Kinnear case in the Washington State Supreme Court (described above)

- Preliminary proposed mathematical algorithm for making taxes equitable for the first cycle

- See our Data Explorer for charts and graphs of countywide assessment and taxation data